The Risk of Implicit Guarantees: Evidence from Shadow Banks in China

Ji Huang, Zongbo Huang, Xiang Shao

Review of Finance, Volume 27, Issue 4, July 2023, Pages 1521–1544, https://doi.org/10.1093/rof/rfac061

The Shadow banking sector creates systemic risk through its interconnectedness with commercial banks. As a critical source of this interconnectedness, implicit guarantees extended by commercial banks to their shadow banking entities as ?nancial support beyond any contractual obligation have received much attention from academics and policy makers since the global ?nancial crisis. Yet, since implicit guarantees are, by de?nition, hard to detect and measure, few empirical works have studied how and why banks provide implicit guarantees.

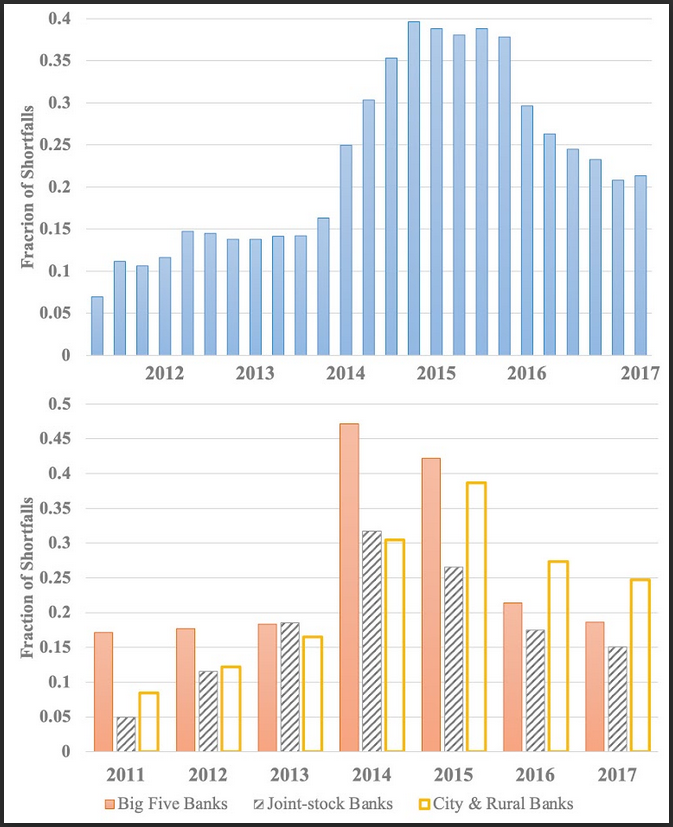

In the paper, “The Risk of Implicit Guarantees: Evidence from Shadow Banks in China,” Ji Huang, Zongbo Huang, and Xiang Shao study the strategic provision of implicit guarantees through the lens of wealth management products (WMPs), China’s largest shadow banking component. The WMP market offers a unique setting to measure implicit guarantees: investors’ return expectations are transparent and observable. Investors expect issuing banks to deliver the target returns announced at issuance. Moreover, although there is no contractual obligation, investors expect banks to “dip into” balance sheets and guarantee the target returns when underlying assets underperform. While banks meet investors’ expectations for most WMPs, realized returns fall short of target returns for approximately 25% of WMPs. Thus, comparing target returns and realized returns at maturity provides a direct measure of implicit guarantees: fewer return shortfalls indicate stronger implicit guarantees. The figure below presents the fraction of WMPs that experienced return shortfalls over time at the quarterly frequency and by bank type at the annual frequency.

The authors show that banks facing higher interbank borrowing rates extend stronger implicit guarantees. A one-standard-deviation increase in the interbank rate reduces the probability of return shortfalls by 3.4 percentage points. The authors also exploit the Baoshang Bank bankruptcy in May 2019 with suggestive evidence. As the negotiable certificate of deposit yields of city and rural banks spiked relative to the Big Five and joint stock banks, city and rural banks extended stronger implicit guarantees and disclosed realized returns more often.

Since the interbank rates capture bank risks perceived by interbank investors, this result implies that, as perceived risks increase, banks become less reputable and have a stronger incentive to build their reputations and reduce rollover costs by guaranteeing the target returns of WMPs. To support this reputation mechanism, the authors also con?rm that when the fraction of return shortfalls in the previous month decreases by ten percentage points, the average realized return of WMPs issued in the current month declines by 3.1 basis points.

The authors show that collectively, banks strategically provide implicit guarantees due to reputation concerns. The results shed light on ongoing regulatory reform: regulators can identify the potential “step-in” risks associated with implicit guarantees with transparent and timely interbank borrowing rates. From the ex-ante perspective, the results suggest assigning higher risk weights to off-balance-sheet entities sponsored by riskier banks in quantity requirements.

Figure