Capital Gains Tax, Venture Capital, and Innovation in Start-Ups

Lora Dimitrova, Sapnoti K Eswar

Review of Finance, Volume 27, Issue 4, July 2023, Pages 1471–1519, https://doi.org/10.1093/rof/rfac057

Entrepreneurial firms supported by Venture Capital (VC) investors play an important role in innovation and productivity growth. VCs are associated with some of the most influential and high-growth, entrepreneurial firms in the world. Given the relevance of VC for firm-level innovation, we focus on the effect of taxation on VC firms’ incentives and the innovation outcomes of start-ups.

So far, studies have not evaluated this question because a large proportion of the partners in VC firms are tax-exempt. However, one category of investors in VC, the general partners (GPs) or partners in charge of managerial decision-making, are not tax-exempt. We argue that an increase in the tax rate on capital gains decreases the return to GPs and therefore reduces their incentives to invest, and support existing portfolio start-ups, and that affects the start-ups’ innovation and success.

This question has broad-based impact because, in the US, VC firms are structured as “pass-through entities”. This means that the firm itself does not pay taxes; the profits are distributed to the partners who pay taxes as a part of their individual tax returns. Such pass-through distributions account for around half of the total realized capital gains in the US. Given that the tax policy on capital gains is arguably one of the more important ones for VC firms, we focus on those taxes.

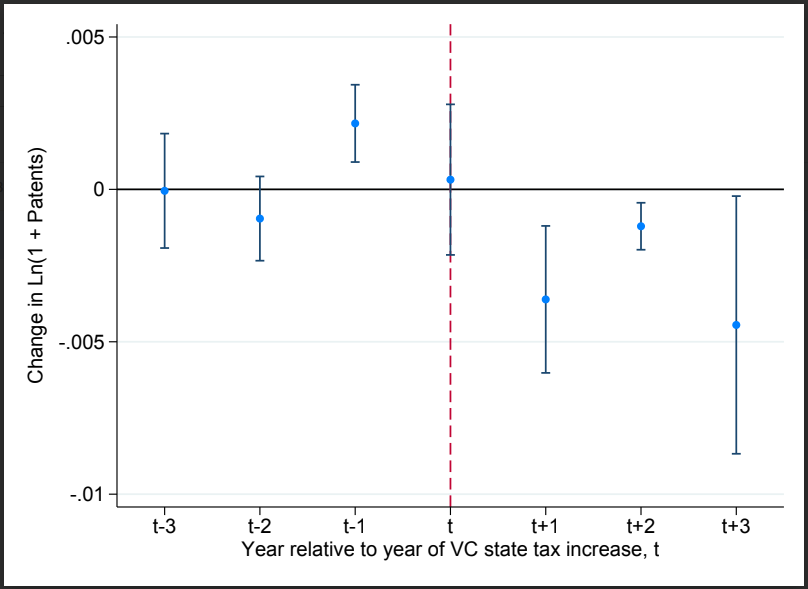

Our focus on VC-backed start-ups has a key advantage. It allows us to disentangle the two channels: the VC channel and the entrepreneur channel. VC firms can respond to increases in taxes by reducing the supply of capital and reducing engagement with start-ups (the VC channel). Entrepreneurs can respond by reducing their demand for capital and their level of risk-taking (the entrepreneur channel). Using detailed geographic information on entrepreneurs and VC firms, we are able to identify these two channels separately. This identification is an important contribution of the paper and provides valuable policy implications. We find that an increase in the capital gains tax leads to a decrease in the quantity and quality of start-ups’ innovations. The elasticity of patents to changes in the capital gains tax of VC firms is –0.45 to –0.75. Our results suggest that incentivizing VC firms to become more actively involved in their portfolio of start-ups could significantly benefit innovation.

We examine the mechanisms behind our main finding. A higher capital gains tax can lead to lower investment by VC firms and consequently smaller portfolios. We document that less investments by VC firms, and investments in fewer firms lead to fewer innovation outcomes.

We also find that increases in the capital gains tax of VC firms lead to incrementally lower innovation exchanges between start-ups in the VC firm’s portfolio. As successful inventions typically benefit from such exchanges, our results suggest that an increase in the capital gains tax of the VC firm can lead to fewer innovation exchanges that thereby lead to fewer innovation outcomes for start-ups.

Figure 1