Olga Balakina, Claes Bäckman, Andreas Hackethal, Tobin Hanspal, Dominique M Lammer

Review of Finance, Volume 30, Issue 3, May 2026, Pages 1029–1069, https://doi.org/10.1093/rof/rfaf077

Family and friends are important sources of advice, including for financial decisions. Recent survey data indicate that 25 percent of surveyed investors rely on information `somewhat’ or `a great deal’ from friends, family, and colleagues when forming investment decisions, comparable to the reliance on financial advisors (27 percent) and significantly higher than information from social media (12 percent). However, despite the prevalence of advice from family and friends, there is limited evidence on the nature and quality of financial advice in close personal relationships, which we refer to as personal financial advice.

This paper offers several novel facts regarding personal financial advice using unique brokerage-level data on social ties and portfolio composition, which we complement with a survey of (unrelated) retail investors. We first use survey evidence to document that 51 percent of respondents who receive financial advice (whom we term Followers) frequently consult family and friends, compared to 13 percent who turn to social media and 20 percent who turn to financial advisors. Followers seek trust and expertise, with few mentioning financial returns. The role of expertise also becomes apparent when examining who provides advice: respondents who typically advise family and friends possess more experience, larger portfolios, and higher self-assessed financial aptitude.

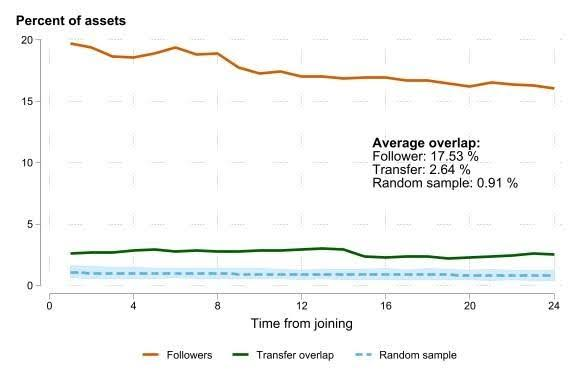

Next, we examine a referral campaign at a large German online bank and brokerage to investigate how personal advice influences portfolio composition. The referral program involves bank customers (Recommenders) inviting acquaintances (Followers) to join the bank and its brokerage. We compare the assets that Followers purchase upon joining the bank to the assets that Recommenders hold in their portfolios. Followers and Recommenders share, on average, 17 percent of securities, a proportion that remains persistently high over a two-year period. The portfolio overlap is consistently higher than any placebo-pair estimate.

We then find a strong correlation between the participation of Recommenders and Followers in funds. If a Recommender invests in funds, her Follower is 49 percent more likely to invest in funds, with larger effects for passive funds than for active funds. Ultimately, Followers choose the same assets as their Recommender and end up with a higher-risk portfolio share, earning higher realized and expected returns, and having better-diversified portfolios than other new investors.

We argue that the personal relationship alters the nature of advice and compels the Recommender to internalize the Follower’s outcomes. This distinguishes our setting from the previous literature, which often involves anonymous or pseudonymous relationships. Incentives for posting on social trading platforms may include the desire to generate interaction and attract followers, necessitating a more active trading strategy.

Our results also highlight a broader issue: financial advice on social media is readily accessible to everyone, regardless of their background, but the quality of such advice is debatable. Personal financial advice from family requires connections to experts, but it is of high quality instead. Understanding who has access to high-quality advice from trusted sources and who instead is left to finding advice on social media is an intriguing question for future research.

Figure 1