Social Interaction in the Family: Evidence from Investors’ Security Holdings

Samuli Knüpfer, Elias Rantapuska, Matti Sarvimäki

Review of Finance, Volume 27, Issue 4, July 2023, Pages 1297–1327, https://doi.org/10.1093/rof/rfac060

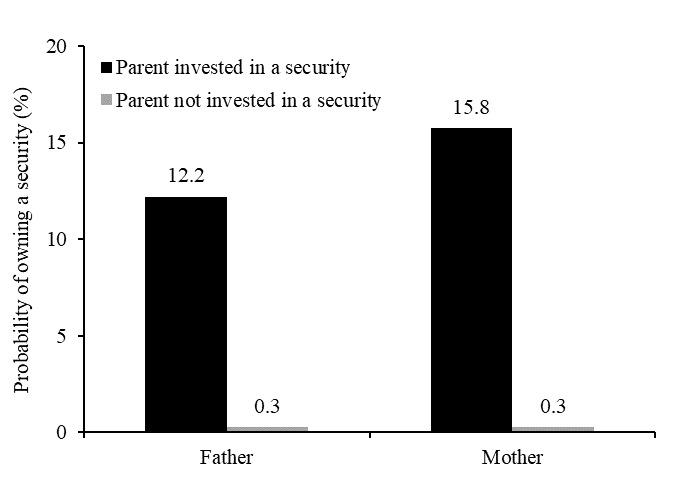

Investors tend to hold the same securities as their parents. Figure I illustrates this fact using register-based data that cover the entire investor population in Finland in 2004–2008. It shows the probability of owning a

stock or a mutual fund is 16% when the investor’s mother owns the same security and only 0.3% when she does not. This difference is also large when the investor’s father owns the security.

Our paper presents evidence suggesting social interaction within the family is an important reason why investors’ choices are correlated with those of their parents. This intergenerational influence has implications for understanding portfolio choice, wealth inequality, and behavioral biases.

We find the previously documented strong intergenerational correlations in portfolio attributes are largely confined to the securities investors share with their parents. This result suggests social forces in adulthood significantly contribute to intergenerational correlations in portfolio choice. Narratives solely emphasizing early-life factors thus leave an important part of the story untold.

We also report shared security holdings exacerbate wealth inequality by increasing the dispersion in the families’ returns on wealth. They can also negate some of the insurance benefits family members could achieve by diversifying across different securities. These findings may thus matter for how insurance motives are incorporated into analyses of within-family decision-making

Finally, shared security holdings appear to propagate behavioral biases from an investor to her family members. This result suggests the aggregate impact of behavioral biases can be larger than that expected in the absence of familial spillovers.

We reach these conclusions using many complementary approaches. We flexibly control for preferences for specific types of assets an investor and her parents may share. We also use two quasi-experimental research designs that are immune to time-variable influences simultaneously affecting investors and their parents. Both approaches strongly support the social-influence hypothesis.

Figure I. Security choice across generations in the entire investor population in Finland in 2004–2008