Roni Michaely, Guillem Ordonez-Calafi, Silvina Rubio

Review of Finance, Volume 28, Issue 5, September 2024, Pages 1575–1610, https://doi.org/10.1093/rof/rfae017

We uncover strategic voting behavior by some Environmental and Social (ES) funds that significantly decreases support for ES proposals when their votes are likely to be pivotal. To mask this behavior, they vote in favor of ES proposals when the proposal is likely to pass or fail by a large margin, inflating their average support for ES proposals, giving a possibly misleading impression about their voting impact on ES issues.

Who does it and why? ES funds are supposed to incorporate ES values into their investment and voting decisions. But at the same time, ES funds in non-ES families are subject to a conflict between the fund stated goals and family preferences: their non-ES family objectives are different, (legitimately) prioritizing profits over ES goals. We find that funds strategic voting pattern, akin to greenwashing votes, allows funds to exhibit high average support for ES proposals, consistent with their stated goals. However, when their votes truly count, they vote against ES proposals in a manner consistent with family preferences. It seems that they are able to hold the stick at both ends.

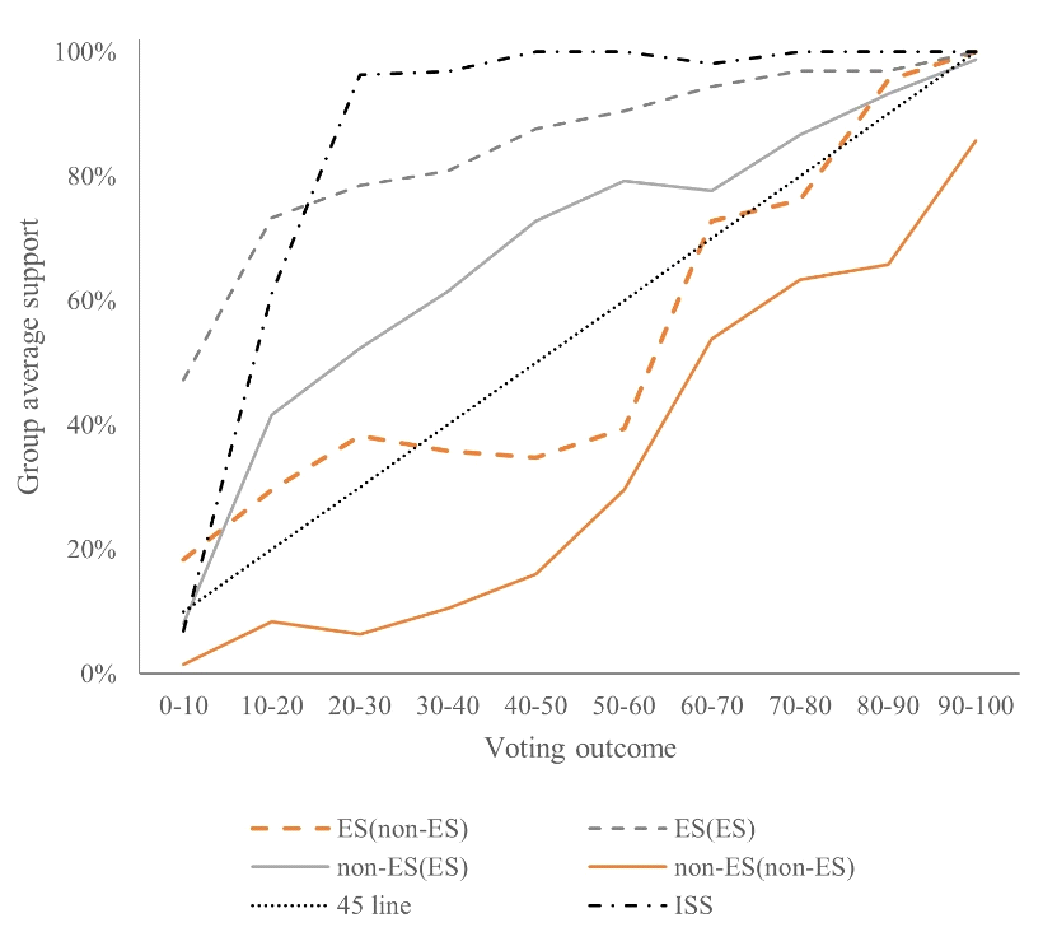

The plot below illustrates this strategic voting. The horizontal axis shows the voting outcome of the proposals, and the vertical axis indicates the average support provided by different groups of funds. The figure shows that ES funds in ES families provide the highest support for ES proposals for all possible voting outcomes, while non-ES funds in non-ES families provide the lowest support. This is in line with what one would expect.

More of a surprise is the voting pattern of ES funds in non-ES families, revealing a U-shaped relationship centered on the 50% approval rate: they are relatively more supportive of ES proposals when overall support is either low or high (above the support of the average investor, as represented by the 45-degree line). Conversely, they vote for ES proposals relatively less when the probability of being pivotal is higher. This pattern is not present for other funds. Not for ES fund of ES families (grey dashed line), for non-ES fund of ES families (grey continuous line), or non-ES funds of non-ES families (orange continuous line). We run numerous robustness tests and find that this unique behavior of ES of non-ES families is robust throughout our various tests.

To summarize, average support masks some important voting pattern that allows funds to vote in a way that is inconsistent with fund shareholders’ best interests. This has implications for regulators and investors. For regulators, our findings indicate that the current disclosure of proxy voting does not always allow investors to monitor votes. For investors, we show that while a fund’s stated ES objectives affect its average voting pattern, the preferences toward ES of the family to which it belongs are also important. Hence, they should consider both dimensions deciding which fund they invest in.