David Hirshleifer, Yushui Shi, Weili Wu

Review of Finance, Volume 28, Issue 4, July 2024, Pages 1275–1310, https://doi.org/10.1093/rof/rfae009

Past research highlights a tension between analysts’ jobs delivering public information to the market versus delivering private information to their clients. On the one hand, analysts often issue overly optimistic stock recommendations to generate trades from a large audience of retail investors (e.g., Malmendier and Shanthikumar 2007; Kong et al. 2021). On the other hand, the literature has found that sell-side analysts provide useful information to a relatively small audience of fund managers via social networks (e.g., Gu et al. 2019; Li, Mukherjee, and Sen 2021). The dual roles of analysts suggest that analysts need to balance the informativeness of their public recommendations against the trading value of their private information.

We perform tests motivated by the idea that analysts give more precise information to fund managers than the recommendation observed by investors. We propose the following analyst recommendation strategy as a function of the analyst’s private information. The analyst pools by issuing a favorable public recommendation about both high and relatively low-value firm types and privately tells the fund client these separate values. Such a pooling strategy (between these two value types) conceals from retail investors some of the analyst’s private information about firm value. In consequence, the connected fund manager who receives information from the analyst profits by buying when the value of the stock is high, and by selling when the value of the stock is low. This is profitable as the market price has not fully incorporated the analyst’s private information. In sum, there is say-buy/whisper-sell behavior.

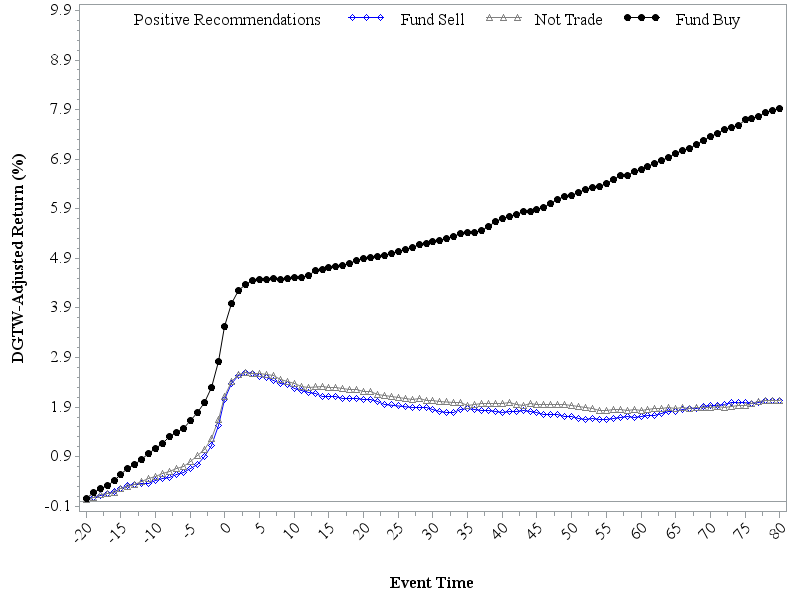

To test for say-buy/whisper-sell behavior, we first identify cases in which analysts’ public positive recommendations are accompanied by selling by connected fund managers. To further distinguish from alternative hypotheses behind fund managers’ selling decisions, we examine the relationship between analysts’ say-buy/whisper-sell behavior and voting by fund managers for analysts in star analyst competitions. We find that managers are more likely to vote for the analysts who exhibit more say-buy/whisper-sell behavior with these managers, apparently as payback for the analysts’ private information. This relationship is consistent with the hypothesis that analysts use say-buy/whisper-sell behavior to give fund managers private and more-accurate information than analysts give to the general public in their public recommendations. We further find that among the analysts’ positive public recommendations, the stocks bought by the managers who vote for the analysts outperform the stocks sold by these managers (see the figure), consistent with managers receiving more-accurate information.

These findings suggest that analysts have incentives to limit the informativeness of public recommendations even under the pressure of government regulation. Furthermore, since analysts’ public recommendations do not reveal analysts’ true beliefs about stocks, the performance of analysts’ public recommendations is an imperfect indicator of analysts’ abilities and career prospects.

Figure: Cumulative abnormal returns around analyst positive recommendations by voting fund trades