Stefano Lovo and Jacques Olivier

Review of Finance, Volume 30, Issue 2, March 2026, Pages 597–637, https://doi.org/10.1093/rof/rfaf060

We model the decision of a Rating Agency (RA) whether to adopt an “issuer pays” or “investors pay” business model, with the aims to explain why Environmental, Social, and Governance (ESG) ratings are predominantly paid by investors while credit ratings are paid by firms, and to analyze the implications of the choice for firms’ expected stock price and ESG performance.

Our baseline model differs from a standard Grossman-Stiglitz (1980) in two ways. First, a fraction of the investors are Socially Responsible (SR) and care about both the firm’s cashflows and ESG performance, while the remaining investors care only about the firm’s cash-flows. Second, we introduce a strategic profit-maximizing RA capable of credibly reporting the firm’s ESG performance. If the RA chooses the “issuer pays” model, the firm must decide whether to pay a fee to have its ESG performance publicly disclosed. If the RA chooses the “investors pay” model, only investors who pay a fee receive the information, while others try to infer it from the equilibrium stock price. Importantly, the model becomes isomorphic to a credit ratings

model when all investors are SR, in which case cash-flows and ESG performance are perfectly substitutable.

ESG ratings impact the expected stock price because they reduce the risk faced by SR investors. The greener the firm (i.e., the better its expected ESG performance) and the larger the proportion of SR investors, the more positive is the impact of ratings on stock price, and thus the larger is the fee that the firm is willing to pay if the RA chose the “issuer pays” model. By way of contrast, because of agents learning from prices, the RA faces a downward-

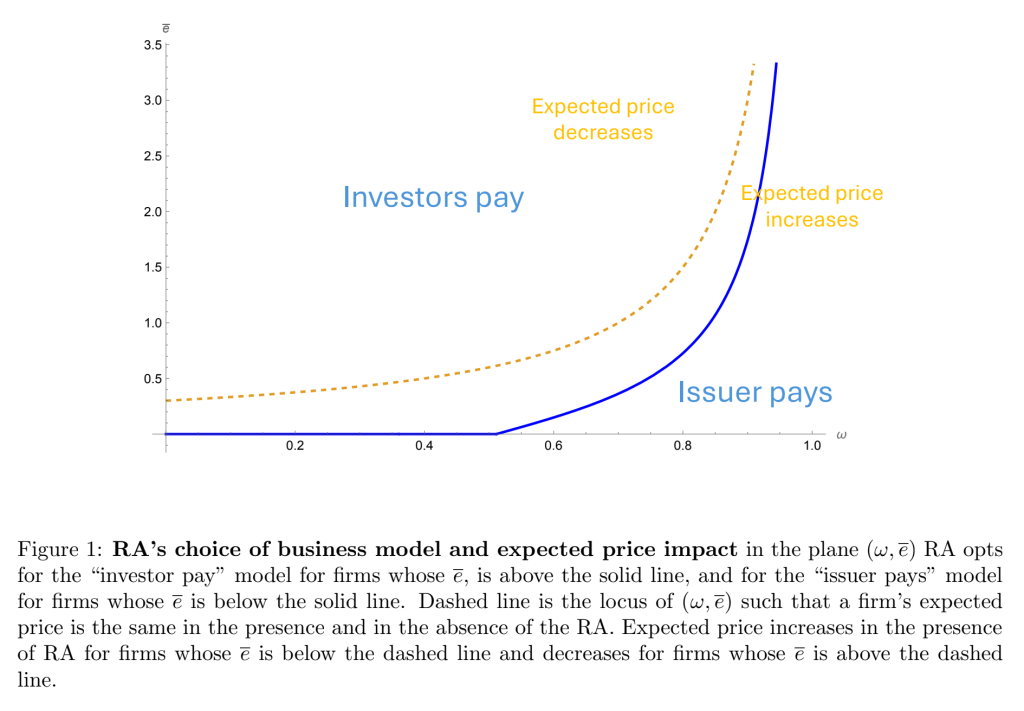

sloping demand for information if it chose the “investors pay” model, which caps its revenue as a function of the proportion of SR investors. This leads to the paper’s central finding that the “issuer pays” model is optimal when firms are sufficiently green or when the proportion of SR investors is sufficiently large. Since the model converges to a model of credit ratings when all investors are SR, our finding rationalizes the otherwise puzzling empirical evidence that credit ratings are purchased by firms while most ESG ratings are paid by investors.

This result is illustrated by the graph below, where the x-axis represents the fraction of SR investors, ?, and the y-axis the ESG performance, with a high ?e corresponding to a worse expected ESG performance ( ?e equal to expected emissions of the firm).

Finally, we extend the model to allow the firm to make an ex-ante investment to improve its expected ESG performance. We show that the presence of an RA increases the firm’s incentive to do so. This is because ESG ratings make the equilibrium stock price more sensitive to the firm’s expected ESG performance. Interestingly, this impact is an inverse U-shaped function of the fraction of SR investors, implying that the real impact of ESG ratings is largest when the preferences of investors in the market are heterogeneous.