Alexander Tuft and Emmanuel Yimfor

Review of Finance, Volume 30, Issue 2, March 2026, Pages 717–756, https://doi.org/10.1093/rof/rfaf057

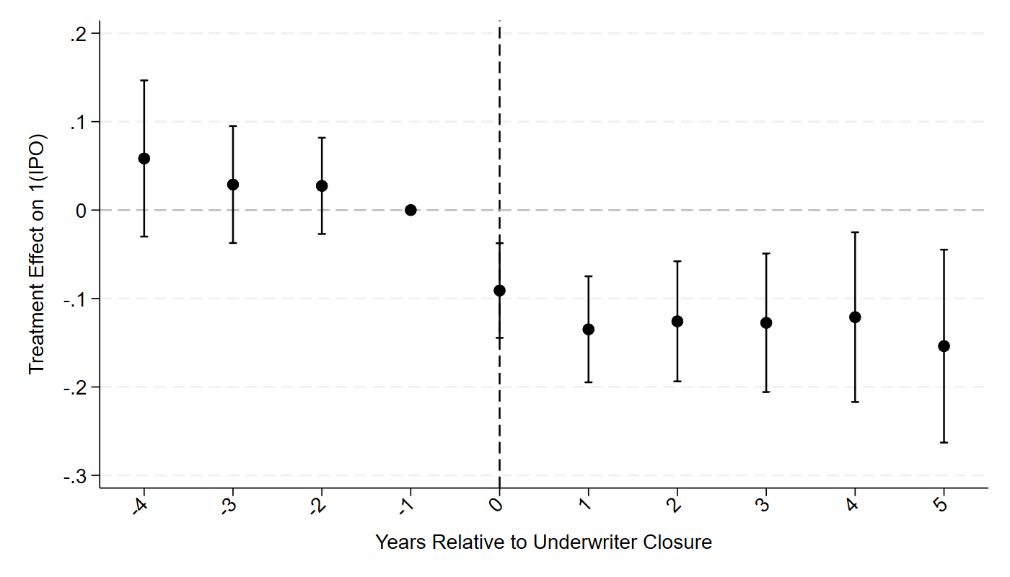

We provide the first causal evidence that relationships between venture capital firms and investment banks matter enormously for accessing public markets. When VCs lose an established underwriter relationship through bank mergers or closures, their IPO exits fall by 9.5% and fund returns drop by 7.8%.

Our identification exploits truly exogenous shocks. The 2008 failures of Lehman Brothers, Bear Stearns, and Merrill Lynch had nothing to do with their underwriting businesses. These premier banks collapsed because of mortgage securities, not IPO problems. Yet VCs connected to these banks saw 20% fewer IPOs than other VCs for years afterward.

Why do these relationships matter so much? The answer is people. When banks merge, 77% of employees leave. The bankers who remain determine whether VC relationships survive. We track 144,771 investment bankers through mergers and find that higher employee retention directly predicts continued VC collaboration with the merged bank. Personal relationships, built over years of repeated deals, cannot be instantly replaced.

The effects hit hardest where theory predicts they should. Smaller VCs lose 43% of their IPO probability versus 35% for larger firms. Funds actively seeking exits suffer more than those still deploying capital. This heterogeneity confirms we’re measuring real economic frictions.

Our findings overturn the conventional view that underwriting services are commodities. In sophisticated financial markets with intense competition, specific relationships between specific people still create enormous value. This matters for understanding financial intermediation, banking consolidation, and how innovation reaches public markets.

Figure