I-Hsuan Ethan Chiang and Xi Nancy Mo

Review of Finance, Volume 30, Issue 2, March 2026, Pages 681–715, https://doi.org/10.1093/rof/rfaf047

This paper introduces a novel two-beta currency pricing model and uses it to analyze currency trading strategies. Literature on currency risk premiums has identified the predominant common factor in currency returns as the “dollar factor,” an equally weighted portfolio of floating exchange rate currencies. Empirically, the dollar factor behaves like a level factor in the cross section: currencies’ betas with the dollar factor, called “dollar betas,” cannot explain the cross-sectional variation in expected currency returns.

The novelty of this paper is to decompose the dollar beta into two betas: beta with dollar-factor risk-premium news (“risk-premium beta”) and beta with dollar-factor real interest rate news (“real-rate beta”). The two news components capture distinct features of currency market returns, and hence the two new betas can explain more cross-sectional variations in currency risk premiums. Our test features time-varying betas and time-varying prices of beta risks. Unconditionally, risk-premium beta is “bad beta,” because it is associated with a significantly positive price of risk of 2.52% per year; real-rate beta is “good beta,” because it is associated with a negative price of risk. Using the countercyclical indicator average forward discount (AFD) to capture changing economic conditions, we find that the price of risk-premium-beta-risk is countercyclical, while the price of real-rate-beta risk is procyclical. The empirical findings are consistent with a no-arbitrage model with precautionary savings and a pricing kernel characterized by two separate global shocks.

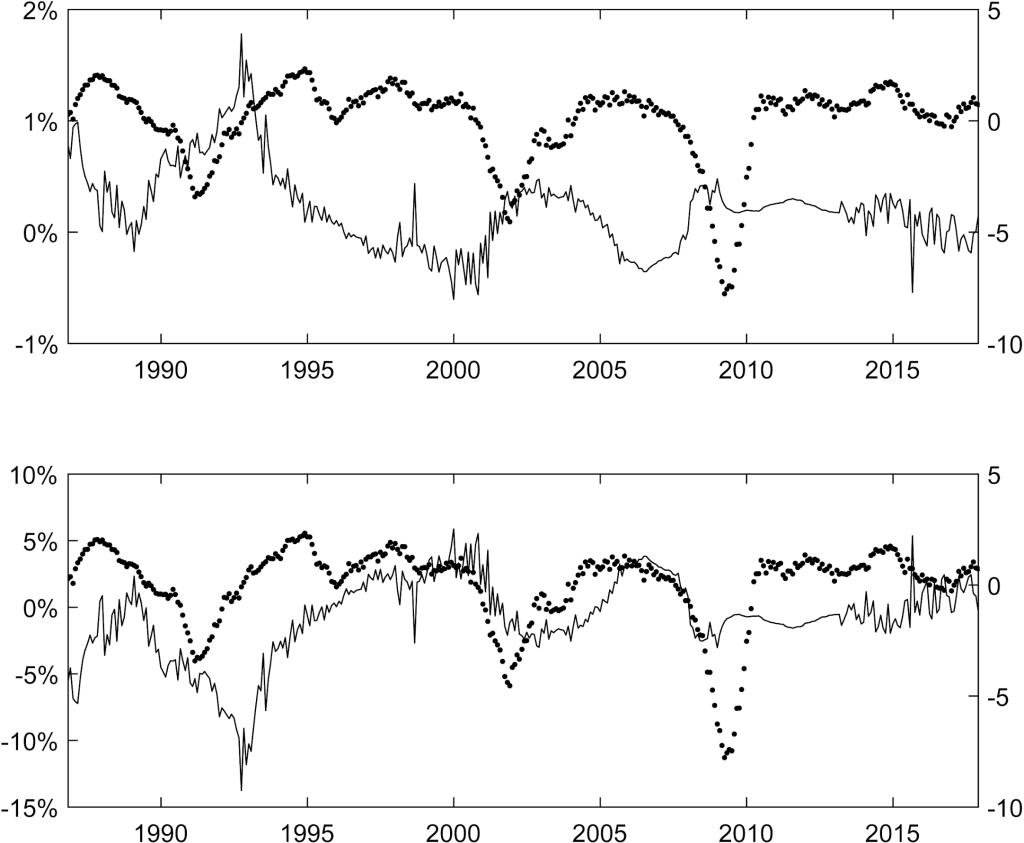

The Figure plots the time series of the prices of risk-premium-beta risk (top panel) and real-rate-beta risk (bottom panel), shown as solid curves and scaled to the left axis. For comparison, the real activity is indicated by the dotted curve in both panels, scaled to the right axis. The Figure illustrates that the price of risk-premium-beta risk is countercyclical, while the price of real-rate-beta risk is procyclical.

We then utilize our estimation results to analyze the performance of a number of notable currency trading strategies, and we find that most currency trading strategies either have excessive “bad beta” or too little “good beta,” failing to deliver abnormal performance. At the same time, a spurious alpha can be detected in a single-factor model with only the dollar factor, or in a two-factor model with the dollar and the carry factors.

To verify that precautionary savings are the main economic driver of our results, we switch to other 34 reference currencies, one at a time, and implement our two-beta currency pricing model. Consistent with our baseline results, risk-premium (real-rate) betas are bad (good) betas in developed countries, where precautionary savings prevail. When the home country is an emerging-market country, our U.S.-based results are largely reversed. Note this result is also consistent with our theoretical prediction, because precautionary savings are absent in emerging-market countries.